Datafiles

Jun 24

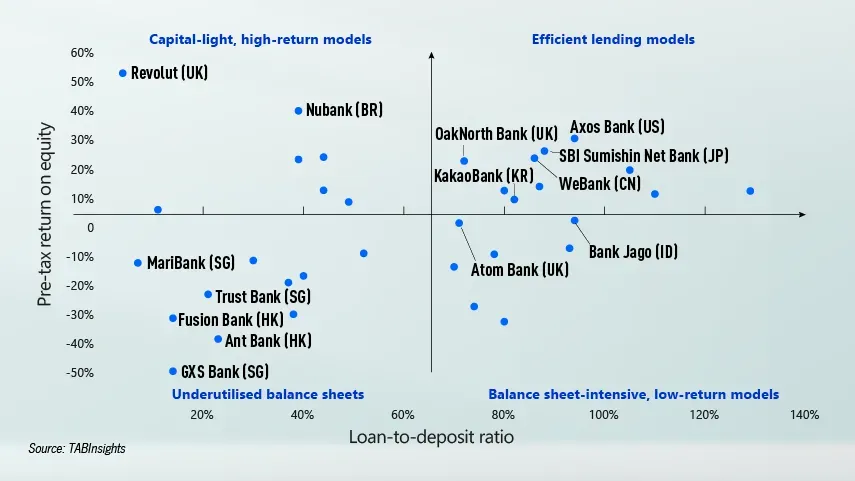

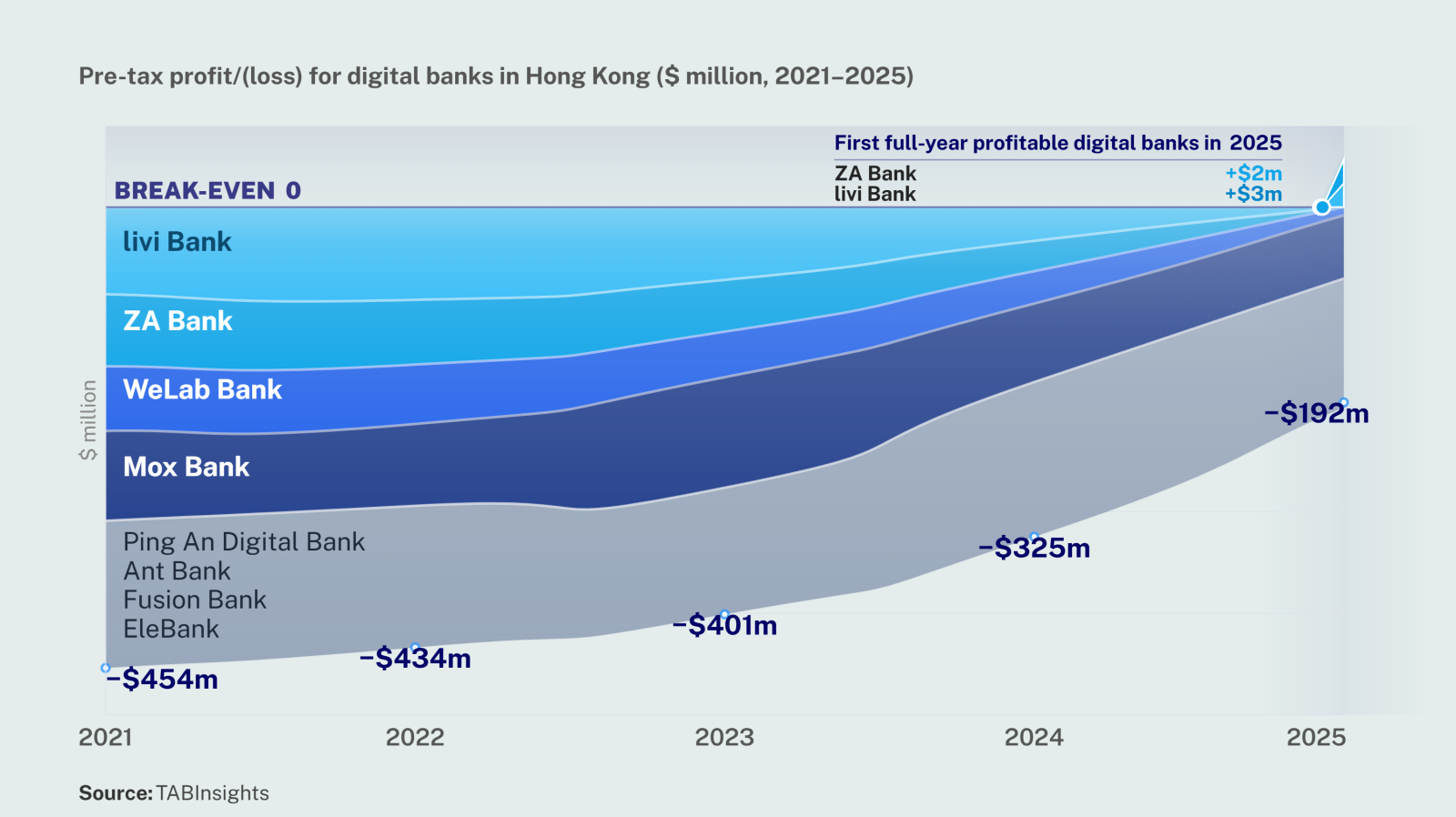

Aggregate losses across Hong Kong's digital banks narrowed sharply, while two leading players, ZA Bank and livi Bank, moved into profitability, supported by an improving revenue mix and tighter cost control, signalling growing progress towards break-even across the sector after more than six years in the market.